Cross posted from The European Tribune.

The Euro celebrates its 10th. Birthday on 1st. January. The exchange rates between the founding currencies were fixed from 1st. January 1999 when the Euro began to circulate in the form of traveller’s cheques, electronic transfers, and banking transactions. The physical banknotes and coins appeared three years later in January 2002.

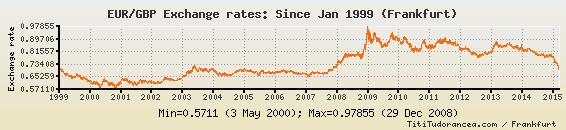

The Euro depreciated rapidly following its introduction (at 71p Sterling) down to a low of 57p Sterling in May 2000 reflecting widespread scepticism (in the Anglo world) that a single currency covering many diverse economies could be stable. It was worth 77p Sterling as recently as mid-October. Today (17th. Dec.) it soared over 93p Sterling (up from 89p since my first Countdown to €/£ parity diary on 12th. December.

Against the dollar, the Euro fell from an introductory value of €1 = $1.18 in Jan-1999 to $0.82 in 2000 and then rose to €1 = $1.57 in Jul-2008, and $1.43 now.

The success of a currency cannot, of course, be The success of a currency cannot, of course, be measured entirely in terms of its exchange rates. Just as important is its stability over time, its credibility in international markets, and the volume of transactions conducted in it. The Eurozone has recently drawn level with the USA as the World’s largest economy (hat tip to DoDo) and may well become by far the largest when up to another 12 potential members join. It may also become the world’s dominant reserve currency if the US $ continues to be as unstable as it has become in recent years.

The Euro has been an almost unalloyed success from the point of view of a small member state such as Ireland. Irish inflation peaked at 24% in the mid 1970’s and early 1980s and I well recall paying 18% interest on my mortgage. This was largely caused by periodic oil and Sterling crises, although it has to be said that high inflationary expectations had also become embedded in the Irish economy and consumer psyche.

Ireland broke the link with Sterling to join the ERM in 1979 ((PDF Alert) at a time when the UK represented 50% of Irish imports and exports and gradually managed to reduce its inflation rates to something closer to the German model – though not without two devaluation crises in 1986 and 1993, which forced the Irish central bank to increase (PDF Alert) overnight interest rates to 100% in order to try to protect the value of the Irish Pound within the ERM. It became obvious that smaller currencies were always going to be extremely vulnerable to speculative international monetary flows way beyond what any small economy or Central Bank could resist. Even one Month interbank rates peaked at 60% and it was clear huge economic damage would ensue if such crises were to recur on a regular basis.

The subsequent currency stability and much reduced interest rates enabled by the ERM and then the Euro was one of the major factors behind the rise of the Celtic Tiger. The one major downside has been that Eurozone interest rates have been far too low for a rapidly growing Irish economy which entered the “bubble phase” of higher consumer price inflation and huge land, house and asset price inflation in recent years. Irish governments didn’t understand that a much more restrictive fiscal policy was required once the traditional remedies of devaluation and domestically controlled interest rates were no long available to policy makers.

Once the bubble burst big time, the ECB was also very slow to recognise the changed realities and actually increased interest rates as recently as last August. So the major downside of the Euro for a small peripheral economy is the fact that interest rate and monetary policies are always going to be set by the major players – Germany and France – in their own interest – rather than taking the needs of smaller peripheral economies into account.

Ireland is now being hit by a triple whammy of a Global financial crisis, a domestic asset price crash, and a major revaluation vis a vis our major trading partner and close neighbour in Britain and Northern Ireland. Irish Goods and services are becoming grossly uncompetitive and losing market share and sales big time to Northern Ireland and internet vendors with domestic October retail sales down 7% on the same period last year. So the rapidly revaluing Euro really isn’t a good thing as far as the Irish economy is concerned, and we would much prefer a lower Euro and lower Eurozone interest rates to try an reflate the Irish economy, asset prices and consumer confidence.

Longer term, however, there is no doubt that the Euro has been a good thing as far as the Irish economy is concerned, and although we face a much more difficult period of adjustment now, there are no calls for a return to the Irish Pound or to a link with sterling. Ultimately, we would much prefer if Sterling joined the Eurozone as well – even at parity – because then, even if there was a huge loss of competitiveness in the short term, at least we wouldn’t be facing 20% swings in exchange rates with our largest market and with all the uncertainty that this entails.

A little more sensitivity by the ECB towards the needs of its more peripheral members would also be much appreciated – especially as the Euro grows to embrace many more small members states – but I hardly expect this to happen. With the prize of becoming the dominant global reserve currency in its sights, the Mandarins of the ECB are hardly going to give the travails of minor peripheral economies like Ireland a second thought.

I will leave an analysis of the pros and cons of becoming the dominant Global reserve currency to the bankers and economists amongst us. Obviously it can be a source of considerable pride and reinforce the positive image of the Euro and the EU as a success. However, as we all know, pride comes before a fall, and perhaps the hubris which accompanied the Celtic Tiger can also act as a cautionary tale for the Eurozone should the Euro become too successful, too quickly.

The inappropriately high Euro exchange which could accompany the Euro becoming the Global reserve currency could also result in a prolonged long term decline of the non-financial elements of EU economies. We rely on our central bankers to ensure that monetary policies reflect real conditions on the ground in the real economy, and not some new Euro centred financial bubble in the future.