Ireland has been producing some fairly decent economic statistics for a couple of years now – despite the general stagnation in the Eurozone and the continuing “consolidation” of the public finances as the Troika imposed austerity plan seeks to reduce the current budget deficit to below 3% by next year. But the latest figures showing 9% GNP growth and 7.7% GDP growth in the last 12 months take the breath away, and even if they prove to be something of an anomaly, would seem to indicate that the Irish economy has reached take-off velocity despite the heavy gravitational pull of public sector spending cuts, a 125% debt to GDP ratio, and stagnant external markets.

About 5% of Irish GNP and GNP can be attributed to the tax avoidance strategies of (mainly US) corporates basing themselves in Ireland for tax purposes, whilst in reality, the vast bulk of their activities take place elsewhere. The

marked divergence between GNP and GDP growth above can also be attributed in large part to the so called “Patent Cliff” which has resulted in a large fall in the value of pharmaceutical exports as blockbuster drugs like Lipator and Viagra come off-patent.

Ireland is the fifth biggest exporter of drugs in the world, and Irish chemical and pharmaceutical exports surged by more than a quarter in the five years to 2011 when they peaked at €56bn, a figure equivalent to almost a third of gross domestic product. But the employment content of those exports is relatively small, and what is clear from these recent figures is that there is a much more broadly based recovery taking place in the Irish economy which is now even making up for the fall in drug export revenues.

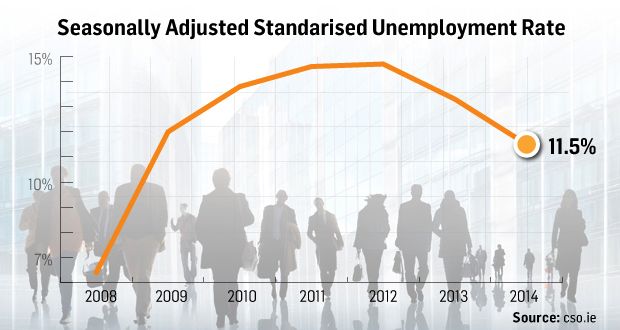

The composition of the Irish workforce has been transformed into a much more knowledge based workforce, and the unemployment rate has declined steadily – from 15 to 11.5% – below the Eurozone average rate of 11.8%, aided, to some extent, by continuing net emigration.

However the size of the total workforce has yet to recover to pre-recession levels and there is controversy as to the actual number of real additional jobs being created:

Property price in Dublin have risen 25% from their bottom at the height of the recession and are now also starting to rise again in the rest of the country prompting some fears that we may be back into a boom and bust property price cycle. However they are still over 30% below their peak at the height of the boom, and there are signs that the construction industry is beginning to ramp up output again from very low levels to meet pent-up demand. These price rises are also helping to reduce the number of households in negative equity and the number mortgages in arrears or in default – which should enable the banks to survive the stress tests due to be published on October 26th.

Partly as a result of this and increased employment levels, consumer confidence is at a 7 year high and private spending is beginning to increase from a low level – even as households continue to deleverage and rebuild their balance sheets after the recession. Government tax revenues are running about €1 Billion ahead of target which means that the c. €2 Billion adjustment which was expected to be required in next months budget to meet the Troika (and EU) 3% deficit target can be met without further tax rises, and indeed some income tax reductions and spending increases are being signaled as forming part of the budgetary arithmetic. The Irish state can now borrow on the markets at O% interest and is negotiating with the EU and IMF to repay bail-out loans early and save c. €400M p.a. in interest payments in the process.

The government remains under pressure to reform its corporate tax code but claims that the 12.5% corporate profit tax rate will become progressively more attractive as all countries are forced to close their corporate tax loopholes. One of the unstated reasons why the Government remained largely silent on the Scottish independence debate was that it feared an independent Scotland would become a more aggressive and successful competitor for FDI. There also appears to be considerable optimism that a British exit from the EU could leave Ireland inundated with banks and other corporations relocating from London to Dublin in an attempt to retain access to the Single Market.

So are we witnessing the emergence of a Celtic Phoenix from the ashes of the Celtic Tiger, or is Ireland once again in the throes of an irrational exuberance which could have a very sorry ending? Certainly the strategy of attracting FDI partly through tax competition has been very successful, at least in the short term, but this is not a strategy which the rest of the Eurozone could pursue without diluting the benefits for all. Ireland’s national debt is due to peak at c. 125% of GDP next year – up from just 25% in 2008 – and this will remain a headwind for the public finances for many years to come. Much of the burden of adjustment during the recession fell on those dependent on state benefits and services and Ireland’s GINI index has yet to recover to pre-recession levels.

It will be some considerable time before the bulk of the people actually feel that the recession is over for them personally, and in the meantime the Government is trying to “manage expectations” by limiting expansionary policies as much as possible until the 2015 Budget where it will have maximum impact on electoral perceptions ahead of the next general election due in 2016. Some will no doubt benefit from improved employment prospects in the meantime, but if you are dependent on state benefits and services your situation will still take quite some time to improve.

As Krugman has noted, if you measure success as any improvement on the disastrous consequences of austerity, you are setting the bar for success very low indeed. Ireland is recovering, but it is from a relatively low base, and it will still be quite some time before those who felt the brunt of austerity the most see any tangible benefits in their real lives.

{kind=link}